About Us

Our Portfolio

Investors

ESG

Media

Data science and managing assets on behalf of partners has taken on growing importance for this owner of shopping centres and retail parks.

A big conundrum in the British commercial world is the future of the high street. Now that department stores are nearly extinct, many streets are surviving on supermarkets, charity shops and women’s fashion stores that are often teetering because too many visitors browse and return home to buy online. Amid much head-scratching, NewRiver’s Allan Lockhart thinks he has a solution: stick to everyday necessities.

His important distinction is between destination centres like Hammerson’s Brent Cross in north London, now being turned into a leisure hub, and NewRiver’s local shopping centres and retail parks serving daily needs. Lockhart says: “We have a very high frequency of visits but lower dwell times compared with a destination shopping centre.”

Not that he would turn down a trophy centre if one came his way, though it would have to be with a partner. “The thing about a big destination shopping centre is the deal size,” Lockhart says. “They can cost £200 million to buy, too much for us alone, so we’re more likely to be doing that in a partnership with a big co-investor.”

Management in its broadest sense is becoming an increasingly important part of the business, handling £1.4 billion of assets on behalf of partners, from private equity funds to local authorities. That produces a tenth of group profits and is growing. It also feeds NewRiver’s burgeoning database.

The company has hired a data scientist and upgraded systems to analyse vast pools of real-time data: footfall, car park usage, mobile phone metrics and quarterly occupiers’ retail sales, aiming to make informed capital allocation choices.

Lockhart founded NewRiver with his father 17 years ago and in 2024 added the complementary Capital & Regional property firm to take the combined portfolio value close to £1 billion. After disposals, that has been trimmed to £802 million, so the group owns or manages 44 shopping centres and 31 retail parks from Edinburgh to Eastbourne, with 43 per cent in London. In the year to March, occupancy was 95 per cent and 99 per cent of rents were duly paid. Its tenant roster includes virtually all the big names, from Boots to Burger King, and 90 per cent of them renew leases.

“Predicting how AI and automation will alter long-term consumer shopping habits is the harder, more interesting challenge,” Lockhart says. “Retail real estate has been disrupted by technology more than any other commercial property sector, so we constantly look a decade ahead.”

The current winners are omnichannel retailers that embrace both physical stores and online trading. The likes of Next and M&S have been taking market share away from pure online operators because of the interactive data benefit. Vacancy rates have fallen in NewRiver’s shopping centres, prompting higher rents, and the outlook is enhanced by an apparent build-up in individuals’ bank savings.

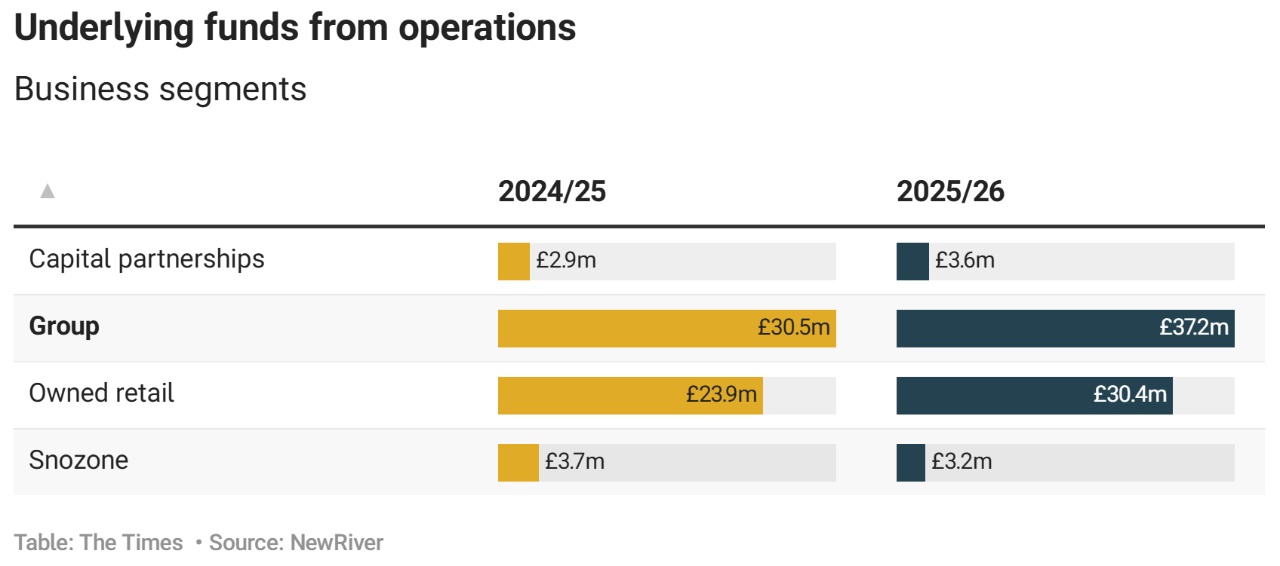

In the year to March, NewRiver’s underlying funds from operations (Uffo) increased 22 per cent to £37.2 million, but Uffo per share, the “clean” cash profit available to pay dividends, rose more modestly from 8.1p to 8.3p. The ratio of net debt to ebitda was a healthy 6.2 times and interest was covered 4.6 times.

The shares are trading at 25 per cent below their net asset value, against the 21 per cent sector average, reflecting NewRiver’s lack of diversity and that its £335 million market value is too small for some investing institutions.

That has also puffed up the dividend yield to 8.7 per cent. Although to qualify for their tax status Reits have to distribute 90 per cent of profits, NewRiver can keep that down to a more conservative 80 per cent because of other activities, bizarrely including three Snozone artificial ski slopes inherited through Capital & Regional.

While Peel Hunt accepts the company’s total accounting return (Tar) was a respectable 9.4 per cent, it rates the shares only a hold because of the potential impact of higher interest rates from £300 million debt refinancing in 2028. However, Jefferies analysts say buy as “all the ratios are sturdy with (loan-to-value) gearing reduced to 40 per cent”.

With no dominant shareholder, NewRiver could be vulnerable to a takeover bid, but its growing management and data-science arms make it more of an intangible people business than an orthodox property play.

Advice: Buy

Why: A well-run business with a solid and generous dividend yield